Upstox Originals

India’s banks are stretching their loan-to-deposit ratios

6 min read | Updated on February 12, 2026, 19:37 IST

SUMMARY

India’s banks are lending faster than they’re collecting deposits, and that gap is now too large to ignore. With loan-to-deposit ratios at record highs, liquidity is getting tighter and trade-offs are emerging. This article explains what’s driving the imbalance, where the risks lie, and why the credit boom may not be as comfortable as it looks.

Stock list

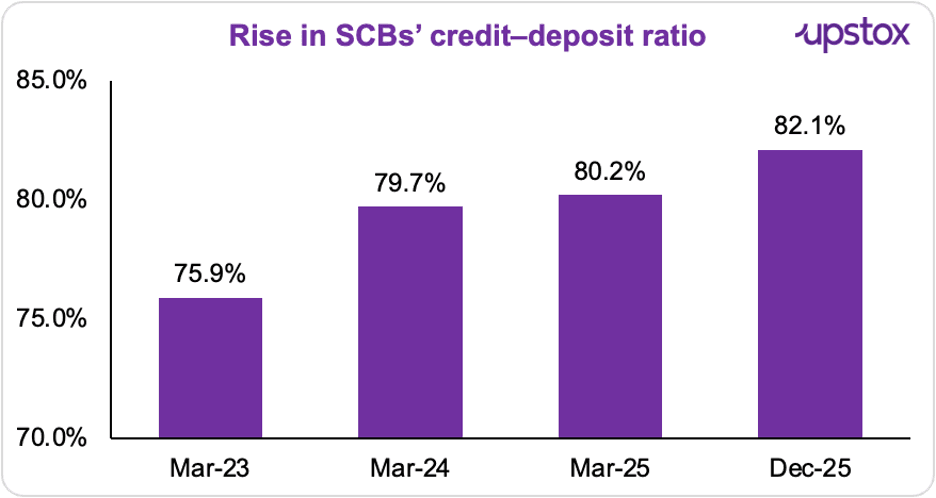

In the December quarter, banks ended up lending out 82.1% of the deposits they collected

At first glance, India’s banks look busy. Loan books are growing, credit demand is healthy, and money is moving through the system.

But.. dig a little deeper and a quiet imbalance shows up.

In the December quarter, banks ended up lending out 82.1% of the deposits they collected, pushing the system’s loan-to-deposit ratio (LDR) to a record high since the 2000s (when it was ~53%).

What’s LDR? It’s a check on how much of a bank’s deposits have already been lent out. Well, high LDRs aren’t new. What’s different now? In earlier credit cycles, high LDRs were cushioned by:

- Strong CASA growth

- Slower digital withdrawals

- Limited competition from market-linked savings

That cushion is thinner now.

Now, according to Bajaj Markets and SBI Research, 70–80% is generally considered the comfort zone.

Source: Care ratings

Several public and private sector banks ended the December quarter with unusually high loan-to-deposit ratios; a quiet but telling sign of stress building on the funding side of the system.

HDFC Bank, the country’s largest private-sector lender, captured this trend most clearly. Its loan-to-deposit ratio edged back uncomfortably close to the 100% mark (for the quarter ending December 2025):

| Bank | Advances (₹ lakh crore) | Deposits (₹ lakh crore) | Advance Growth (YoY) | Deposit Growth (YoY) | LDR |

|---|---|---|---|---|---|

| HDFC Bank | 28.44 | 28.6 | 11.9% | 11.6% | 99.5% |

| Axis Bank | 11.70 | 12.60 | 14.10% | 15.00% | 92.9% |

| Kotak Mahindra Bank | 4.80 | 5.42 | 16.00% | 14.60% | 88.6% |

| IndusInd Bank | 3.18 | 3.94 | -13.10% | -3.80% | 80.7% |

| Yes Bank | 2.57 | 2.92 | 5.20% | 5.50% | 88.0% |

| RBL Bank | 1.04 | 1.19 | 13.00% | 12.00% | 87.4% |

| Bank of Baroda | 13.44 | 15.47 | 14.57% | 10.25% | 86.9% |

| Union Bank of India | 10.16 | 12.22 | 7.13% | 3.40% | 83.1% |

Source: Whalesbook

Are banks already showing strain? There’s no system-wide stress yet. So, It’s about building a safety shield early, before funding pressures have a chance to snowball.

Why is this happening?

As households chase better returns, money that once sat in savings and current accounts is steadily moving into equities and mutual funds. With markets performing well and mutual fund assets under management jumping 35% YoY in FY25, bank deposits are no longer the default choice. This shift could intensify if the Reserve Bank of India cuts rates further, making deposits even less attractive.

The impact is already visible. CASA now accounts for about 37% of total deposits, down from 42% in March 2022.

At the same time, overall deposit growth has slipped into single digits, even as loan demand has picked up. Bankers aren’t optimistic about an easy turnaround either. Amitabh Chaudhry, MD and CEO of Axis Bank, recently described deposit mobilisation as a “hard grind” for the sector.

With CASA shrinking, term deposits now make up 60–65% of liabilities, growing at around 13% but at yields of 6–7%. That has lifted banks’ cost of funds by 15–25 basis points, quietly squeezing margins. Even large private lenders like HDFC Bank have seen CASA slip to around 35%.

What are the consequences?

When deposits are tight, rate cuts don’t travel very far.

With the credit-to-deposit ratio at record levels, banks may be forced to raise deposit rates to attract funds, pushing up their cost of capital. If they don’t, deposit growth risks slowing further; leaving banks with even less room to lend.

That creates a problem for monetary policy. The Reserve Bank of India’s Monetary Policy Committee has already cut rates by 125 basis points in 2025, bringing the repo rate down to 5.25%. But banks struggling to mobilise deposits can’t easily pass on these cuts without weakening their funding base.

Another consequence of sustained high loan-to-deposit ratios is a tilt toward higher-yield unsecured lending. RBI data shows that unsecured retail loans such as personal loans and credit cards accounted for about 51.9% of incremental retail NPAs as of December 2024, highlighting where early stress tends to emerge when credit growth outpaces deposits.

It tightens liquidity headroom. A persistently high CD ratio indicates that most deposits are already deployed as loans, leaving banks with limited surplus liquidity.

So, will the credit–deposit ratio stay high?

Most probably.. and that’s why it matters.

Credit demand is expected to remain strong. GST rationalisation, lower interest rates and income-tax incentives are encouraging households and businesses to borrow more. Loan growth, in other words, isn’t the constraint.

Deposits are. Household savings are weakening, while money continues to shift toward market-linked instruments like equities and mutual funds.

And this is where a key nuance comes in.

CRR and SLR are regulatory minimums, not usable liquidity buffers. They ensure compliance, but they don’t provide much day-to-day flexibility when most deposits are already deployed as loans. At high credit–deposit ratios, surplus liquidity on bank balance sheets is thin.

That’s why elevated LDRs matter. They make banks more sensitive to slower deposit growth or sudden withdrawals. To keep lending, banks may have to raise funds at higher costs or liquidate assets faster, squeezing margins and weighing on profitability.

What are banks doing?

They aren’t slamming the brakes. They’re changing lanes.

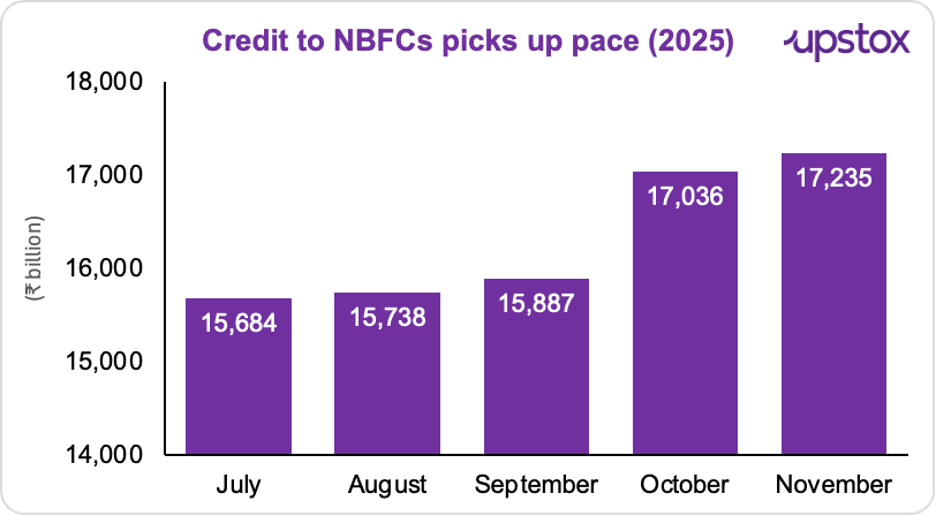

So banks are getting picky about lending from their own books. Instead of cutting off borrowers, banks are increasingly lending to NBFCs themselves. How? Through term loans and working capital facilities.

These NBFCs then handle the last-mile lending to households and small businesses, especially in retail and MSME segments.

Source: CRISIL

This keeps credit moving through the economy. Growth doesn’t stall.

But here’s a thing. The Reserve Bank of India, in its December 2025 Financial Stability Report, flagged this growing interconnectedness as a top-tier risk. If stress builds up in NBFCs; particularly in unsecured loan segments; it won’t stay contained there. The impact would transmit back to banks through their funding exposures.

Way forward

This isn’t stress yet. It’s caution.

With loan-to-deposit ratios staying high, banks have less room to stretch their balance sheets without being careful.

So banks are adapting. And so is regulation.

From April 1, 2026, new Liquidity Coverage Ratio (LCR) rules for digital deposits will kick in. In simple terms, banks will now have to keep more emergency cash against deposits that can be withdrawn instantly through mobile and internet banking, since these deposits are more likely to leave quickly during stress.

While the Reserve Bank of India has capped the extra buffer at 2.5%, the signal is clear: funding risks in a digital world are more structural than before.

Put together, banks now need to focus less on how fast they lend, and more on how safely they fund that lending.

By signing up you agree to Upstox’s Terms & Conditions

About The Author

Next Story